INTRODUCTION

There’s no doubt that a purpose-built token standard is better as it can give issuers and investors the confidence to invest and trust that blockchain technology and standards can handle the complex requirements and regulatory real estate would need.

However, here is the first question I would love to get an answer to:

“Is real estate better a fungible token or a non-fungible token?”

Well, this article has all of my findings.

Fungible can be seen as stocks and bonds; the best thing about fungible tokens or asset is that they can be liquidated as soon as you want to sell.

The most famous and used fungible token standard is ERC 20.

However, non-fungible tokens have a little liquidating problem; an investor must indicate interest by biding a particular asset or token since all the tokens are unique or an owner listing for sale before transactions can happen.

The most used non-fungible token is the ERC 721; its liquidation issue has led to the fractionalisation of such tokens to increase liquidity flow and lower the bearer for investing.

TABLE OF CONTENTS

THE INFRASTRUCTURE UNDERLYING REAL ESTATE TOKENIZATION

Real estate is a huge asset class worldwide. Tokenizing real estate will make it easier for investors especially retail investors to have access to expensive real estate assets, reduce transaction costs to enter the market, cut out middlemen, and make information more widely available.

However, to do this, we need a common standard that accounts for the real-world characteristics of the asset while remaining flexible enough to adapt to various jurisdictions and regulatory environments.

The ERC 20 token standard cannot serve the real estate industry because ERC 20 governs utility tokens.

But for it to be fungible, it will have to be served by a security token with a similarity of ERC20. Like that of ERC-1400 or ERC-1462.

SECURITY TOKEN STANDARDS

Security can represent a share of stock ownership in a company or real estate.

TYPES OF SECURITY TOKENS

The following are the three different categories of security tokens available in the market:

- Equity Tokens

- Debt Tokens

- Asset-backed Tokens

ASSET-BACKED TOKENS

These digital assets have characteristics similar to any commodity, such as gold, real estate, art, and carbon credits; these traded tokens bring value to their underlying asset.

Tokens representing ownership of assets are becoming very popular.

Blockchain has the potential to make a trusted record of transactions; it reduces fraud and improves settlement time, thereby becoming a natural fit for the commodities trade.

In a Proof of Stake (POS) blockchain, tokens are created through a formalised process of distributed validators.

When a purely-digital NFT (ERC-721 token) is transferred, the new owner has a cryptographic ownership guarantee enforced by a validator through a consensus of validators.

For real estate, transfer of ownership is done through legal contract agreements between both parties with property law support.

With existing EIP-721 tokens, transferring the token to another individual does not necessarily impact the legal ownership of the physical asset.

With real estate being tokenized, a balance between the two would be put in place, ownership of tokenised real estate will be enforced and secured by a validator, the legal contract agreement will be transferred to the new owner as well and while smart contracts become the law supporting this transfer and transactions

A DEEP DIVE INTO SECURITY TOKEN STANDARD

The adoption of security tokens, like many new technologies, will be influenced

by standardization.

For security tokens to reach their full potential, issuers and investors must work within an agreed-upon framework; KYC/AML providers and wallets must work with exchanges; regulators must work with developers; and all parties must agree on how they will interact with one another.

Different ERC standards have been developed or upgraded out of existing ones.

Standards like ERC-20 and ERC-721 can be seen as required for most other standards, such as ERC-3525 is a combination of EIP20 and EIP 721; even the ERC 721 requires EIP165.

Security tokens were original, supported by their own unique smart contract on the Ethereum blockchain.

However, issues like consistency in how these smart contracts were engineered and increased friction with process stakeholders like custodians and exchanges, who would need to complete business and technical due diligence on assets.

Challenges like this increased operational requirements unnecessarily when issuing, trading, or managing security tokens, risking the market relevance for a whole new class of assets.

Since many EIPs are coming from the respective backing companies, they capture many excessive niche requirements for a general case.

While security tokens like ERC 1442 require EIP-20, EIP-1066 and ERC-1400 are designed to be compatible with existing token standards, such as ERC-20 and ERC-721.

This can be used in conjunction with other Ethereum-based technologies, such as smart contracts and decentralised exchanges.

ERC-1400 proposes a modular approach to token standards, allowing developers to add or remove functionalities depending on the specific use case.

Some of its proposed functionalities include compliance with relevant regulations such as KYC/AML requirements or transfer restrictions; issuance of security tokens, including the ability to issue tokens in batches and define the number per batch; lock-up periods or limits on the number of tokens that can be transferred at once; investor management features such as whitelisting addresses or blacklisting them, tracking the number of tokens owned by each investor and so on.

This standard was proposed by the Polymath team in 2018, and they later built Polymesh, a purpose-built blockchain for securities.

AN ANALOGY OF ERC1400(ST20) BY POLYMATH TEAM

Token holder 0xabc has 100 TORO tokens which she wants to transfer to her friend 0x123.

0xabc will use her favourite wallet to initiate a transfer by inputting her friend’s ETH address and how many tokens she wants to send her.

Since TORO is an ST-20 token, before the transfer can occur, it will internally call verifyTransfer.

In turn, verifyTransfer uses the GeneralTransferManager’s whitelist to determine if the transfer between these two accounts can happen.

GeneralTransferManager will check 3 things before approving the transfer:

1) That both sender and receiver are in its internal whitelist

2) That 0xabc (seller) is not subject to sale restrictions imposed by securities laws

3) That 0x123 (buyer) is not subject to purchase restrictions imposed by securities laws

If the above conditions are met, the verifyTransfer check is passed, and the transfer transaction can be performed.

As mentioned above, the security token has been designed modularly and allows for the creation of additional modules to extend or modify its own behaviour.

For example, multiple Transfer Managers could be attached to it to control the transfer logic on different exchanges.

ERC-1404 functions enable token issuers to enforce compliance with regulatory requirements, such as verifying the identity of token holders and enforcing transfer restrictions.

It was designed to comply with various securities regulations, including anti-money laundering (AML) and know-your-customer (KYC) regulations and restrictions on who can hold the tokens.

ERC-1404 tokens can also enforce transfer restrictions, meaning that tokens can only be transferred to whitelisted accounts, which can help prevent fraudulent transfers.

But it is also a much simpler base standard as it doesn’t provide enough clarity to distinguish between different ERC-20 transfer functions like transfer and transferFrom .

The standard was proposed by the token issuance platform TokenSoft in 2018.

ERC-1462 is a proposed Ethereum token standard that introduces a new type of token called “partially fungible tokens.”

These tokens differ from traditional ERC-20 tokens because they have unique attributes or characteristics, even if they all have the same value.

For example, a PFT could represent fractional ownership in a real estate property, with each token having a different share of the property’s value.

ERC-884 is a non-fungible token (NFT) representing ownership in a specific real estates asset, such as a property or a plot of land.

Each ERC-884 token is unique and can be verified on the Ethereum blockchain, providing a secure and transparent record of ownership.

One of the key benefits of ERC-884 tokens is that they can enable fractional ownership of real estate assets.

This means that multiple investors can own a stake in a property, with each investor holding a certain number of ERC-884 tokens representing their ownership share.

ERC-884 was proposed by blockchain-based real estate investment platform Harbor in 2018.

SECURITY TOKENS NOT YET ADOPTED FOR REAL ESTATE TOKENISATION

This may not have been adopted, but it is an important step forward in the development of token standards for regulated securities exchanges

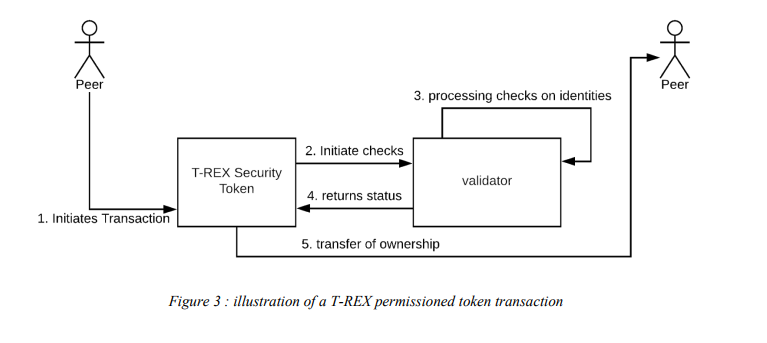

The T-REX standard is built on top of the ERC-1400 token standard, which includes additional functionalities. Some of these include transfer restrictions, investor management and compliance with securities regulations.

T-REX adds additional functionalities to ensure compliance with regulatory requirements for security tokens.

An Illustration of T-REX Permissioned Token Transaction

Source: T-REX Whitepaper

ERC-6065: is a token standard proposed for real estate assets but is still in draft stage. It is proposed to be an interface for real estate NFTs that extends EIP-721.

CONCLUSION

Each of these token standards has its own unique features and advantages, but they all aim to enable the tokenisation of real estate assets, which can provide benefits such as increased liquidity, fractional ownership, and reduced transaction costs.

In other words, the token standard for tokenising real estate will depend on various factors, such as the specific requirements of the real estate project and the regulatory environment in the jurisdiction where it is located.

That being said, ERC-884 is a token standard specifically designed for real estate asset tokenisation.

It includes features such as non-fungible tokens (NFTs) representing ownership in a specific real estate asset, transfer restrictions, and compliance checks to help ensure that tokens comply with applicable securities laws and regulations.

And also ERC 1400, The Polymath ST-20 token standard, may also be suitable for tokenizing real estate assets. It is designed to enable the creation of security tokens that comply with securities laws and regulations.

ERC 1400 token standard includes features such as compliance checks, investor restrictions, and transfer restrictions to help ensure regulatory compliance.