OVERVIEW

Before the advent of DeFi applications built with smart contracts, investors in this space were known primarily for holding tokens, awaiting price rises to make profits.

Might come off as boring, right?

Well, that was the nature of the DeFi ecosystem at the time.

Most DeFi investors always looked up to presales and ICOs because getting in early in these projects was the only sure way to make a profit; this led to the ICO boom in 2017.

In this article, we will explore some of the different sustainable yields in DeFi, such as veToken and real-world assets.

TABLE OF CONTENTS

WHAT IS DEFI YIELD?

In the early days of DeFi applications like Maker, Dydx, Uniswap, and Compound.fi, these decentralized platforms could only attract and maintain contributors in these protocols by providing yields.

These yields acted as a reward for their contribution and also as incentives for risking their assets.

Protocols would split their revenue (transaction fees) with contributors because they took part in the risk-sharing and provision of the assets used for trades on the platforms.

In the case of Compound, Maker, and Dydx, these contributors are known as Lenders.

In the case of Uniswap and Pancake Swap, they are known as LPs.

These contributors provide their assets to these protocols for them to service other users, such as borrowers in the case of Dydx and Compound and Dex traders in the case of Uniswap and Pancake Swap. This brought about the concept of DeFi yield and yield farming.

DEFI YIELD FARMING

Yield farming simply involves contributing assets to protocols for yields, either by staking, providing Liquidity, or lending.

This eventually became the most popular and lucrative activity in the DeFi ecosystem.

People didn’t have to hold tokens any longer to make profits but could also commit those tokens to protocols and receive payment per block or epoch.

This made the whole DeFi ecosystem lively and soon led to a DeFi boom.

DEFI SUSTAINABLE YIELD

Sustainable yield in DeFi became a popular term as soon as it became apparent that most protocols were incentivizing with valueless tokens or over-promising rewards.

As soon as there were drawbacks in the market, protocols couldn’t keep up with their rewards. Some platforms over-promised to boost strap liquidity quickly.

Protocol tokens also lost value due to low demand; this, in turn, reduced the value of additional incentives that are paid out tokens.

This kind of situation exposed poor Protocols with poor token design, which was initially hidden by speculations of token prices by investors.

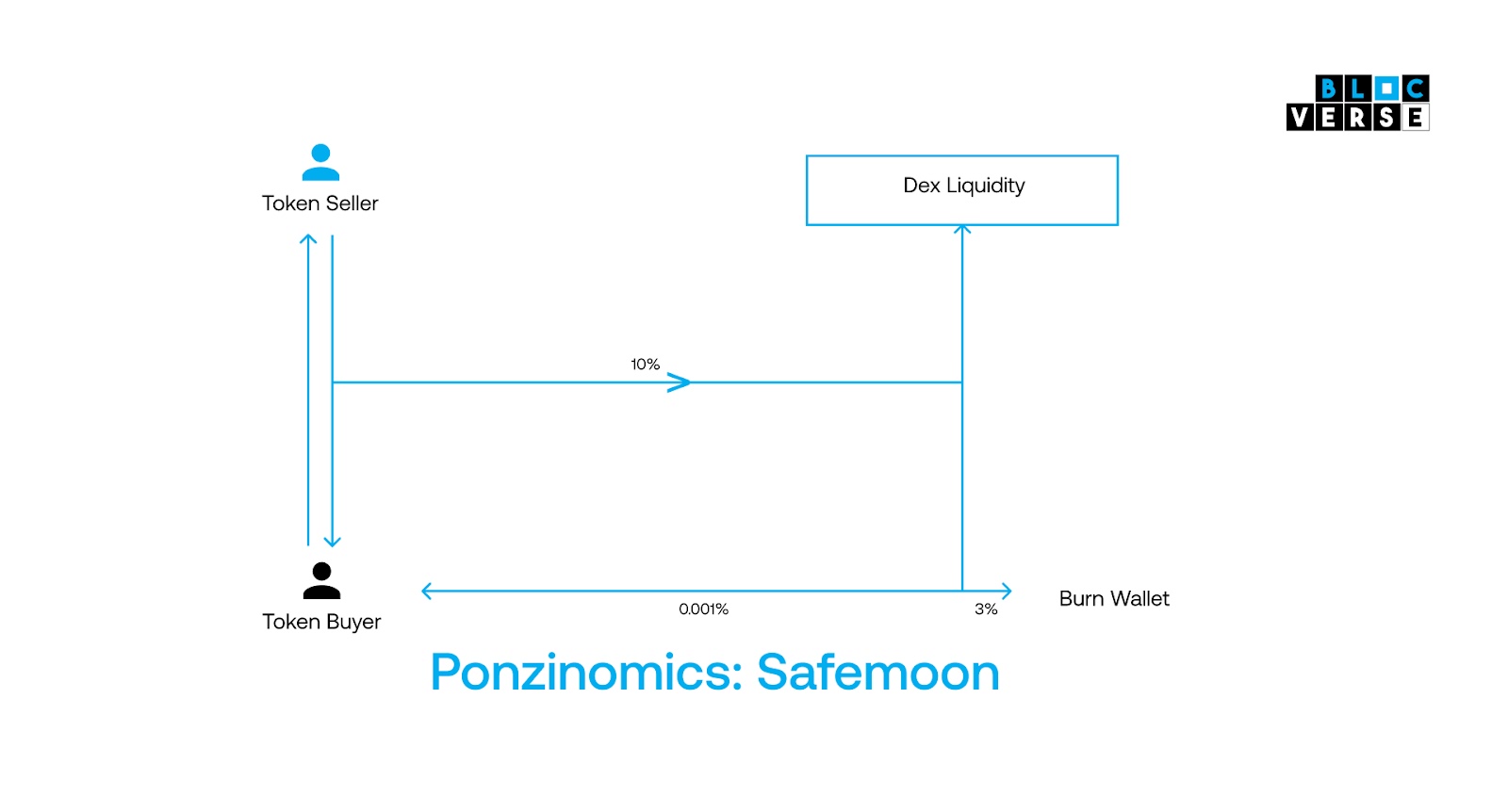

Source: Tokenomics / Ponzinomics case study: SafeMoon by Roderick Mckinley.

Apart from Safemoon being identified as a Shitcoin, its token design was dependent on speculations.

Safemoon had a 10% tax on both buyers and sellers, which was designed to fund liquidity, reduce supply (burn) and reward holders as well.

This alone was not enough to sustain the entire system because as soon as token demand dropped, the reward for holding the token dropped with it.

Besides SafeMoon, most protocols believed they could maintain demand by promising more rewards beyond what the system could generate.

These rewards, however, weren’t real. They were based only on speculation and ponzinomics.

A sustainable yield is a realistic yield – an incentive that would not break the protocol or token design regardless of market conditions. Every protocol should operate like a business.

If the returns for providing liquidity or lending are greater than the interest or fees generated by the protocol, then emissions are dilutionary; this means that the yield is not sustainable or, in lay terms, “real.”

Dilutional yield is not entirely bad since it is a strategy for bootstrapping a new protocol, but needs to be executed properly; if not, it could harm and destroy the reputation of the platform forever.

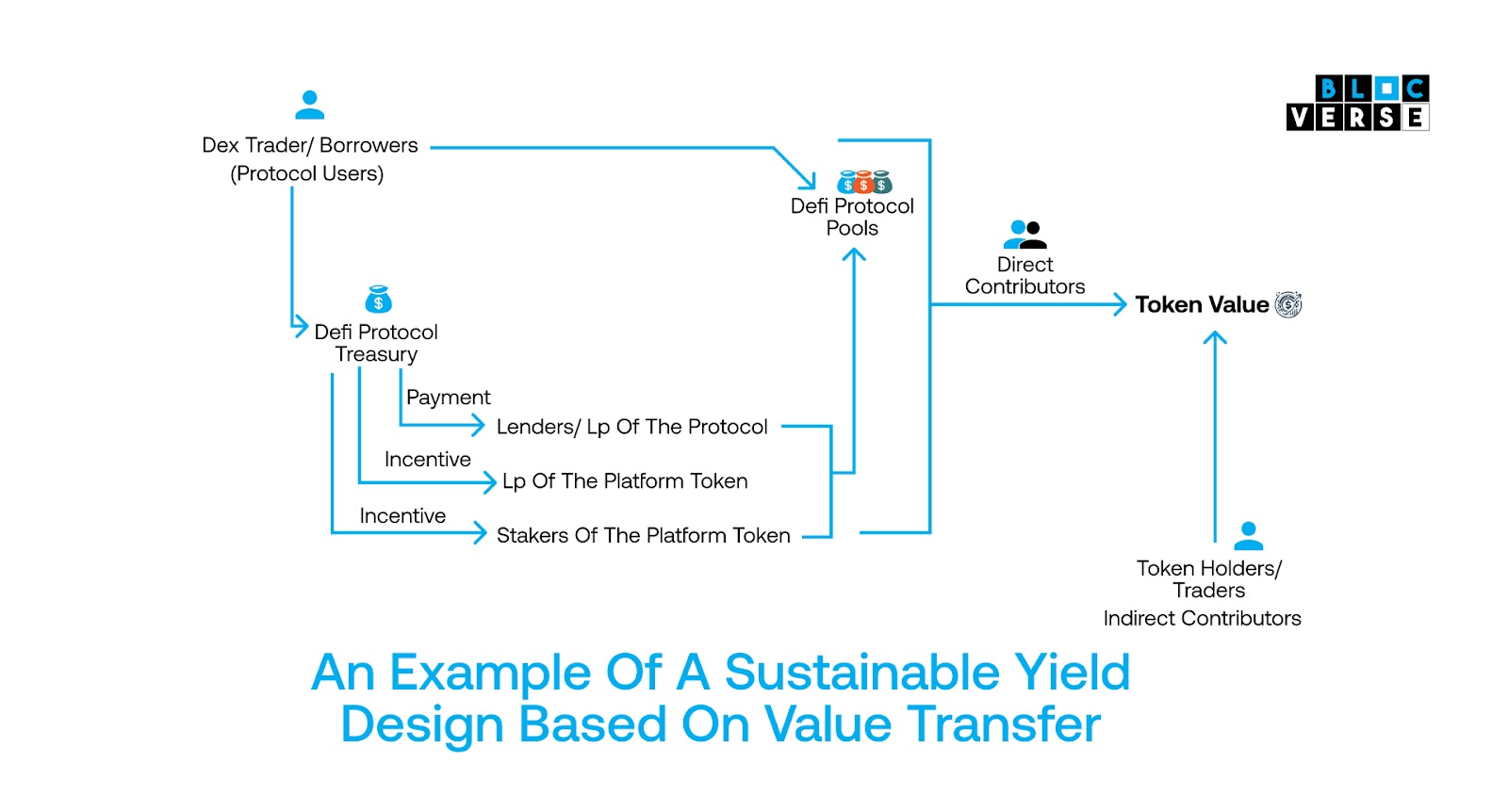

DIFFERENT SUSTAINABLE YIELDS IN DEFI

This design was inspired by Curve Finance.

This protocol was designed so that there is no sell pressure on the token at any point in time, and fees generated from protocol users are shared with protocol contributors according to their risk exposure, leading to a more stable system.

One example of a DeFi protocol that offers real yield is Curve, a stablecoin AMM that allows users to swap between different pegged assets with low slippage and fees.

Curve rewards its liquidity providers with CRV tokens, which can be locked to receive veCRV tokens. veCRV holders can participate in the protocol’s governance and claim a share of the trading fees generated by Curve.

The trading fees are Curve’s main revenue source, and they are sufficient to cover the CRV emissions, resulting in a positive real yield for veCRV holders.

The Curve token design is called veToken, a concept pioneered by Curve’s CRV token. It was designed to better align the users and the protocols through long-term decision-making and commitment. By locking their tokens, users demonstrate their loyalty and interest in the protocol’s success, and in return, they gain more influence and rewards.

Another example is GMX, a decentralized perpetual exchange that offers up to 20x leverage on various crypto assets.

GMX rewards its liquidity providers and traders with GMX tokens, which can be staked to receive veGMX tokens.

veGMX holders can govern the protocol and earn a portion of the protocol fees derived from the interest paid by leveraged traders.

The protocol fees are higher than the GMX emissions, leading to a high real yield for veGMX holders.

HOW DEFI PROTOCOL IS USING REAL-WORLD ASSETS TO CREATE REAL SUSTAINABLE YIELD

Real-world assets (RWAs) have become one of the buzzing sectors and fast-emerging spaces in the DeFi world.

The DeFi ecosystem has been exploring new means to bring value and liquidity on-chain.

It’s quite early to predict the outcome, but the RWA concept is multifaceted, including the tokenization of houses, bonds, stocks, and businesses.

This aims to bring value on-chain and increase the traceability of these assets.

Protocols like Goldfinch lend stable currency to real-world businesses.

Businesses provide off-chain collateral; once they have established credibility with protocol auditors, they make a proposal that contains the payment schedule and yields for investors to consider and invest in.

MakerDao has ventured into the real-world assets space with their periodic investment in Treasury bills, strengthening the stability of the Dai stablecoin.

The U.S. Treasury bond is currently at 5% APY. MakerDao, therefore, stands to earn interest from its on-chain borrowers while also earning 5% on off-chain U.S. Treasury bills.

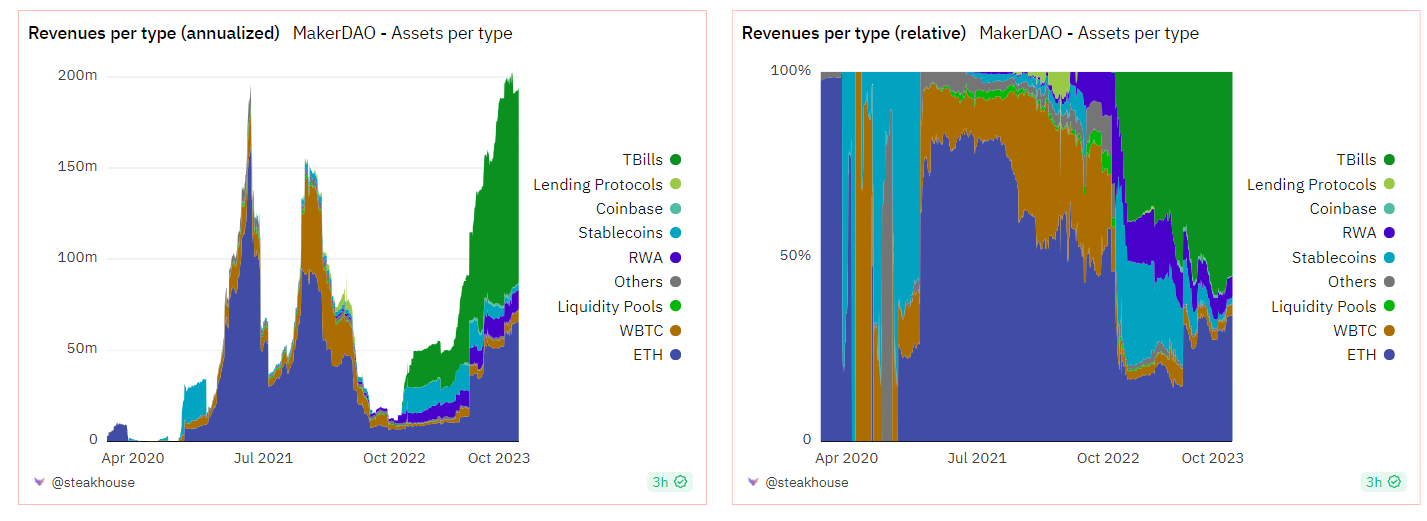

Data from Dune Analytics shows that MakerDAO now boasts a $2.34B RWA portfolio, including $2.6B worth of U.S. Treasury bonds, 500M on other RWA, and 500M of Coinbase.

They all account for about 61% of Maker’s DAO revenue. Maker has also initiated a buyback and burn mechanism for their native token, MKR.

MakerDao Revenue for different revenue segments. Source: @Steakhouse

The MakerDAO protocol aims to maintain a buffer of 50M DAI.

When the surplus surpasses this buffer, the excess is used to buy back and burn MKR, indirectly incentivizing MKR holders and providing a more stable and reliable yield for its lenders and the protocol as a whole.

$MKR buyback progress: Source makerburn.com

Centrifuge another DAO, allows asset originators to tokenize their assets, such as invoices, royalties, or loans, and issue them as non-fungible tokens (NFTs) on the Centrifuge Chain.

These NFTs can then be used as collateral to borrow stablecoins from DeFi platforms such as MakerDAO and Aave, bridging the real world and the crypto economy.

Maple Finance is a decentralized lending platform that connects institutional borrowers with crypto lenders.

Maple Finance rewards its lenders and pool delegates with MPL tokens, which can be staked to receive veMPL tokens.

veMPL holders can govern the protocol and earn a portion of the protocol fees derived from the interest paid by the borrowers.

CONCLUSION: RISKS ASSOCIATED WITH DEFI

The DeFi space is increasingly focusing on sustainability. There is a noticeable decline in the number of Ponzi-like protocols emerging as investors become more aware of the risks associated with protocols promising high yields.

It’s crucial to recognize that, despite the promise of real and sustainable yields, there are inherent risks in these protocols.

These risks include

Smart Contract Risk: The code of DeFi platforms can contain bugs or vulnerabilities, leading to potential exploitation and loss of funds.

Regulatory Risk: The evolving regulatory environment for DeFi can impact the legality and operation of these platforms.

Market Risk: Investment in DeFi is subject to market volatility, with the value of assets fluctuating.

Liquidity Risk: DeFi platforms may face liquidity challenges, making withdrawing funds during market downturns or panic selling difficult.

It’s important to understand how different protocols handle and mitigate these risks. This helps you make more financial decisions.