INTRODUCTION

In the insurance world, where trust, transparency, and efficiency are paramount, smart contracts have emerged as a revolutionary tool.

Smart contracts, built on blockchain technology, are self-executing contracts with the terms of the agreement directly written into code.

These digital agreements are transforming the insurance industry by streamlining processes, reducing fraud, and enhancing customer satisfaction.

Smart contract insurance has the potential to revolutionize the insurance industry. Nevertheless, several factors may hinder the widespread adoption of smart contracts.

The functionality of a smart contract is governed by technological processes, enabling the execution of payments and other actions through rule-based operations. Smart contracts operate independently, without the need for human intermediaries or centralized operators.

This article will delve into the extensive benefits of smart contracts for insurance companies, policyholders, and the industry.

TABLE OF CONTENTS

BRIEF OVERVIEW OF SMART CONTRACTS AND THR BUSINESS OF BLOCKCHAIN TECHNOLOGY

Smart contracts represent a groundbreaking innovation enabled by blockchain technology, leaving a significant imprint on the business landscape.

These computer programs define the terms of an agreement and autonomously enforce them once predetermined conditions are met.

You can read more on smart contracts here.

To grasp the essence of smart contracts, it’s essential first to comprehend the role of blockchain. While Bitcoin often dominates discussions about blockchain, the technology offers diverse applications.

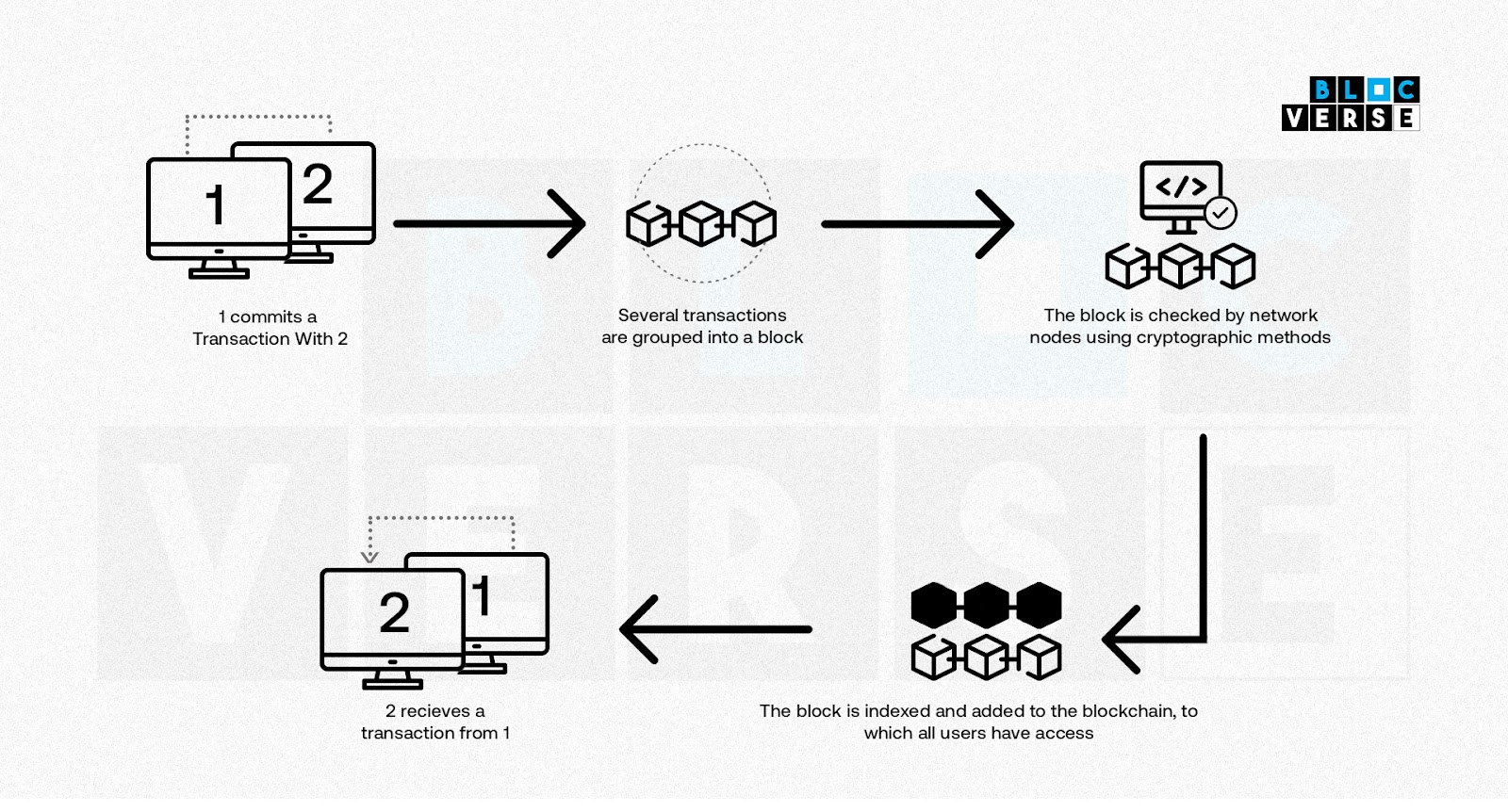

Blockchain technology facilitates decentralized data storage, ensuring that all transactions are executed automatically through code without the interference of third parties.

Providing both security and reliability, blockchain guarantees the immutability of each transaction.

Transactions are seamlessly linked in a chain, with Ethereum emerging as the primary platform for creating and executing smart contracts in today’s landscape.

Read more about the blockchain technology here.

SMART CONTRACTS FOR INSURANCE

Blockchain-based smart contracts offer promising solutions to many of the longstanding challenges the insurance industry faces, grappling with numerous uncertainties and a need to rebuild public trust.

According to YouGov polls, the sentiment towards insurance companies in the United States is mixed, with 47% of Americans expressing trust, while 43% remain skeptical.

While customers often perceive insurers as striving to minimize payouts, insurance companies face challenges.

Policyholders frequently commit fraud, submitting false claims to obtain payouts, leading to mutual mistrust.

Smart contracts have the potential to re-establish trust and render intermediaries obsolete.

These intelligent insurance codes incorporate software algorithms capable of eliminating administrative barriers, predefining all possible insurance payout scenarios, and automatically enforcing contract terms, eliminating room for manipulation on either side.

SMART CONTRACTS DEVELOPMENT STAGES FOR INSURANCE COMPANIES

Creating a smart contract can appear daunting to many insurance organizations, and this apprehension is well-founded.

However, if insurers aspire to develop advanced, customer-centric products, they should understand what’s involved in smart contract development.

Without delving into intricate technical details, the following phases provide a broad overview of how to construct a smart contract:

1. Designing a Token: To build smart contracts, the Ethereum network permits users to craft their tokens for executing specific functions. The key lies in accurately defining which functions to execute and incorporating the appropriate business logic.

2. Implementing the Smart Contract: Ethereum offers a virtual environment called the Ethereum Virtual Machine. Ethereum smart contracts are constructed using Solidity, a high-level, object-oriented programming language tailored explicitly for smart contract implementation.

3. Testing: Smart contracts must be deployed to the blockchain network for execution, but this can pose challenges in terms of testing. Autotests provide a valuable solution by simulating a natural environment and verifying that the smart contract operates as expected.

4. Acceptance and Review: While no formal verification standards exist for smart contracts, there are specialized environments where developers can assess their smart insurance code and logic. An honest review and acceptance process should encompass factors like cost-effectiveness, involving multiple reviewers, and offering transparency in terms of results.

5. Deployment: The next step involves deploying the smart contract to the Ethereum blockchain, making it accessible to everyone. Specific tools can expedite deployment, but generally, engineers must submit the contract code to the blockchain, where the transaction awaits mining. Once mined, the contract is considered deployed.

6. Support: For an insurance company utilizing blockchain technology, it’s essential to have in-house or outsourced resources to maintain the infrastructure of their smart contracts.

BENEFITS OF SMART CONTRACTS IN INSURANCE

Here are the benefits of smart contracts in insurance:

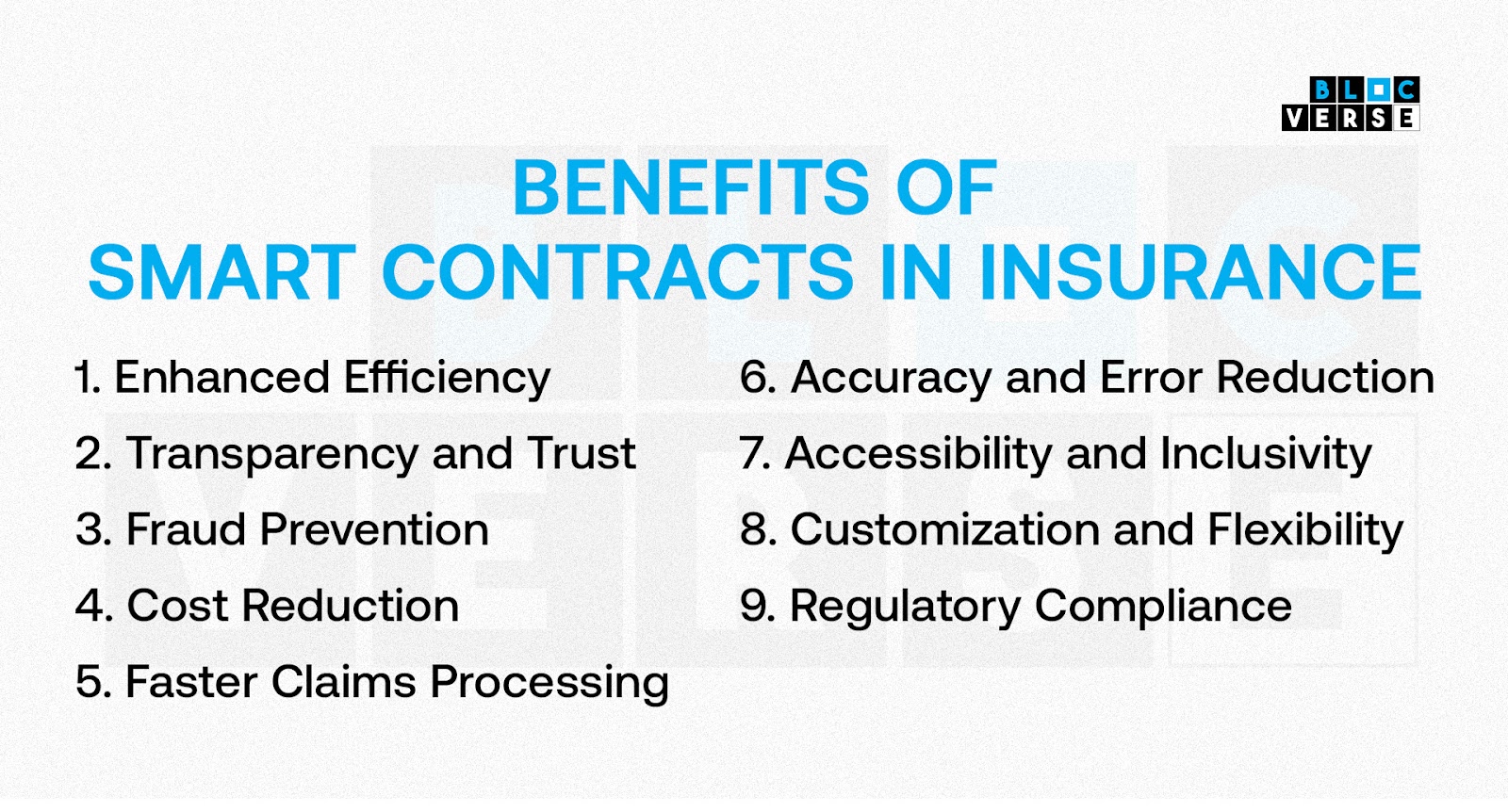

1. Enhanced Efficiency

One of the primary advantages of smart contracts in insurance is their significant boost in efficiency. Traditional insurance processes involve a multitude of intermediaries, paperwork, and manual verification.

With smart contracts, policy issuance, premium payments, and claims processing can all be automated. This eliminates the need for intermediaries, reduces administrative costs, and speeds up transactions.

Policyholders can receive instant approvals and claims settlements, improving their overall experience.

2. Transparency and Trust

Transparency is a cornerstone of the insurance industry, and smart contracts offer unprecedented levels. All terms and conditions of a policy are encoded in the blockchain, making them immutable and accessible to all relevant parties.

Policyholders can confidently review their coverage, premiums, and claims processes, knowing that the contract’s execution is automatic and tamper-proof. This increased transparency builds trust between insurers and policyholders.

3. Fraud Prevention

Insurance fraud is a persistent problem that costs the industry billions of dollars annually. Smart contracts can play a vital role in combating fraud by automating verification processes.

For instance, claims can be automatically validated against predefined criteria, and payouts can be triggered only when the conditions are met. This reduces the likelihood of false claims and encourages honest policyholders.

4. Cost Reduction

Implementing smart contracts can lead to substantial cost reductions for insurance companies. Insurers can significantly reduce administrative and operational expenses by eliminating intermediaries, reducing paperwork, and automating processes.

These cost savings can be passed on to policyholders through lower premiums or used to improve the company’s profitability.

5. Faster Claims Processing

Claims processing is a critical aspect of insurance, and delays can lead to customer dissatisfaction. Smart contracts enable near-instant claims processing.

The contract can automatically trigger the claims, and a payout is made when predefined conditions are met, such as a health diagnosis or an accident report.

This eliminates lengthy approval processes and ensures that policyholders receive their funds when they need them the most.

6. Accuracy and Error Reduction

Human errors in data entry and processing can lead to costly mistakes in insurance. Smart contracts operate based on predefined rules and conditions, significantly reducing the likelihood of errors. Policyholders can have confidence that their policies and claims are processed accurately, leading to greater customer satisfaction.

7. Accessibility and Inclusivity

Blockchain technology and smart contracts can extend insurance services to underserved and remote populations. With the digitization of contracts and payments, insurance can become more accessible to individuals who previously had limited options. This inclusivity can help bridge the insurance gap in various regions, promoting financial security and risk management for more people.

8. Customization and Flexibility

Smart contracts can be highly customizable to suit the specific needs of policyholders. Insurers can create policies with different terms, conditions, and premium structures. This flexibility allows insurers to cater to various customer needs, from basic coverage to highly specialized policies.

9. Regulatory Compliance

Compliance with insurance regulations is a fundamental requirement for insurers. Smart contracts can embed regulatory requirements into their code, ensuring policies and claims adhere to legal and compliance standards.

This reduces the risk of regulatory violations and penalties.

CHALLENGES FACING SMART INSURANCE CONTRACTS

While significant enthusiasm surrounds blockchain technology, it remains widely misunderstood by the general public.

This lack of understanding also extends to harnessing smart contracts as a comprehensive business solution.

Here are some of the concerns that hinder the broader adoption of smart contracts:

1. Limited Scope: Translating simple contractual agreements onto a digital platform can be challenging. Many businesses initially create basic smart contract models following the traditional ‘if X happens, then Y follows’ formula.

2. Complex Technology: Developing sophisticated smart contracts for insurance requires programming expertise. Initially, only experts well-versed in Ethereum can craft functional contracts. This complexity stems from the newness of the technology and the need for a deep understanding of software development.

3. Coding Quality Matters: Smart contracts can be intricate and hard to comprehend. They must be executed sequentially, meaning even the absence of a single critical component can prevent a contract from executing. Despite the goal of reducing human intervention, the development of smart contracts still necessitates human involvement to ensure accuracy.

4. Legal Uncertainty: Smart contracts have garnered substantial interest from public institutions, yet they remain largely unregulated, leading to legal uncertainties surrounding their use.

CONCLUSION

Smart contracts are revolutionizing the insurance industry by enhancing efficiency, transparency, and trust while reducing costs and fraud.

They offer a win-win situation for insurers and policyholders, streamlining processes, improving accuracy, and providing faster claims processing.

As blockchain technology continues to mature, smart contracts will likely play an increasingly central role in the future of insurance, shaping a more accessible, efficient, and customer-friendly industry.

Embracing this technology represents a forward-thinking approach that can benefit all stakeholders in the insurance ecosystem.