INTRODUCTION

The majority of people are aware of the idea of lending and borrowing, whether it takes the shape of mortgages, student loans, or other similar financial instruments. It is one of the foundational elements of the financial system, in fact. Lenders provide money to borrowers under the condition that they repay the money borrowed plus interest.

However, compared to conventional banks and Centralized Financial platforms, DeFi lending and borrowing offers advancements in terms of efficiency, accessibility, and transparency. Regarding loans and borrowing in DeFi, this article covers a wide range of information.

THE CONCEPT OF LENDING AND BORROWING IN DEFI

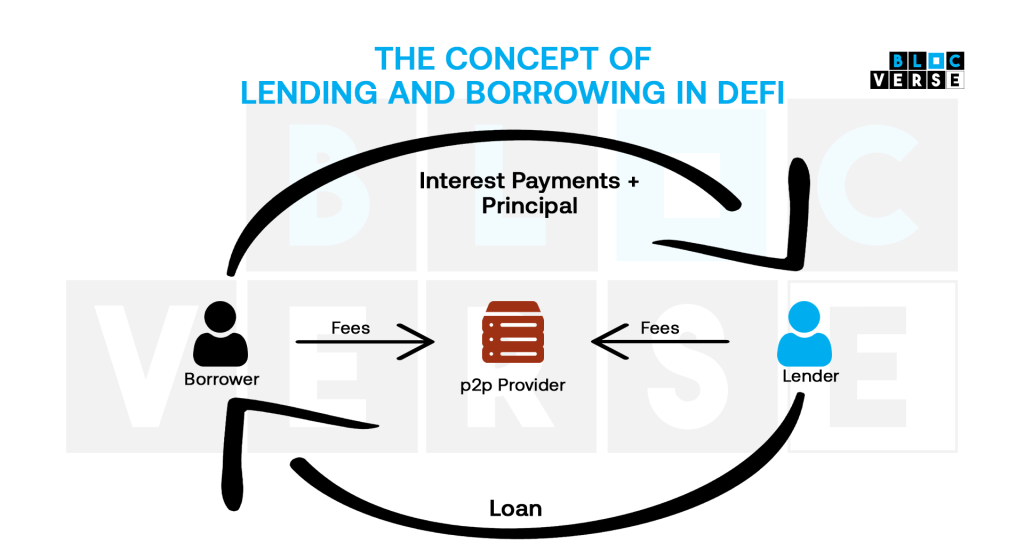

In the environment of decentralised finance (DeFi), lending and borrowing are related to the process of individuals advancing their digital assets to other individuals or borrowing digital assets from other individuals without the need for intermediaries such as banks.

Lending in DeFi generally involves depositing digital assets into a smart contract or a lending platform, which is then made available for borrowing by other users. The lender earns interest on the amount of assets they have deposited, which is paid out in the form of cryptocurrency.

Borrowing in DeFi involves adopting or acquiring digital assets from a lending platform by locking up collateral in a smart contract. The borrower typically pays interest on the borrowed assets, and the collateral is automatically released back to the borrower once the loan is repaid.

One of the main advantages of lending and borrowing in DeFi is that it is more accessible and less expensive than traditional lending and borrowing through banks or other financial institutions. This is because there are no intermediaries involved, and fees are typically lower.

Another advantage is the transparency and security provided by blockchain technology. The lending and borrowing transactions are recorded on a public ledger, and smart contracts ensure that the terms of the loan are automatically enforced, reducing the risk of fraud or default.

Overall, lending and borrowing in DeFi offer a new way for individuals to access financial services and earn interest on their digital assets while also providing opportunities for borrowers to obtain loans without the need for traditional intermediaries.

HOW LOANS WORK IN DEFI

In decentralised finance (DeFi), loans work like traditional loans; however, there are key differences. DeFi provides and manages loans through smart contracts on a blockchain network rather than through centralised financial institutions like banks.

Here are the general steps involved in obtaining a loan in DeFi:

- Collateral: The borrower first needs to provide collateral in the form of a digital asset, usually a stablecoin, which is held in a smart contract as security for the loan.

- Loan request: The borrower then makes a loan request by specifying the amount they want to borrow and the terms of the loan, such as the interest rate and repayment period.

- Loan approval: The smart contract checks if the collateral is sufficient to cover the loan amount and approves the loan if all conditions are met.

- Loan disbursement: The loan amount is transferred to the borrower’s wallet address once the loan is approved.

- Repayment: The borrower must repay the loan amount plus interest to the smart contract by the specified deadline. If they fail to do so, the collateral is liquidated to cover the loan amount and any fees.

RISKS INVOLVED WITH LENDING AND BORROWING IN DEFI

Lending and borrowing on decentralised platforms are becoming increasingly popular, offering many benefits to users, such as access to financial services without intermediaries, transparency, and potentially higher yields. However, there are also risks involved that users should be aware of before participating in DeFi lending and borrowing. Here are some of the most significant risks:

- Smart contract risks: DeFi lending and borrowing platforms operate on smart contracts that execute automatically based on predefined rules. If these contracts contain vulnerabilities or bugs, it can lead to the loss of funds or manipulation of the platform. Smart contract audits and reviews can help reduce this risk, but complete security is not guaranteed.

- Market risks: DeFi lending and borrowing platforms often rely on cryptocurrencies and tokens that are volatile in nature. Fluctuations in prices can result in significant losses for borrowers and lenders, and there is no protection against this risk.

- Liquidity risks: DeFi platforms rely on sufficient liquidity to operate effectively, but if liquidity becomes insufficient, it can lead to high transaction fees, failed transactions, and potential losses for users.

- Counterparty risks: In DeFi lending and borrowing, users lend and borrow directly from one another without intermediaries. This means that users need to trust each other, which can be difficult when interacting with anonymous parties. Default risk can also be an issue, as borrowers may be unable to repay their loans, leading to losses for lenders.

- Regulatory risks: DeFi lending and borrowing are currently largely unregulated, which means that users may be exposed to legal and regulatory risks. Governments and regulatory bodies are beginning to pay more attention to DeFi, and there is a possibility of increased regulation and enforcement in the future.

BORROW LIMITS IN DEFI

In decentralised finance (DeFi), there are generally no strict limits to how much one can borrow, as the lending protocols are typically permissionless and accessible to anyone with an internet connection and a compatible wallet. However, borrowers should be aware of some practical limits and considerations.

Firstly, borrowers must have sufficient collateral to back their loans. In most DeFi lending protocols, borrowers must provide collateral worth more than the amount they wish to borrow. The amount of collateral required varies depending on the protocol and the type of asset being used as collateral.

For example, some protocols may require a 150% collateralisation ratio, meaning that a borrower must provide $150 worth of collateral for every $100 they borrow.

Secondly, there may be practical limits to how much a borrower can borrow based on the liquidity of the market and the availability of the asset they wish to borrow. If there is limited liquidity for a particular asset, it may be difficult to borrow a large amount without significantly affecting the asset’s price.

Finally, individual DeFi lending protocols may impose their own limits on borrowing based on factors such as the borrower’s creditworthiness and the health of the overall lending pool. For example, a protocol may limit the amount a borrower can borrow if their credit score is below a certain threshold or if the lending pool has become overextended.

Overall, while there are no strict limits to borrowing in DeFi, borrowers should be aware of the practical limitations and risks involved in borrowing and should exercise caution and careful consideration before taking out a loan.

HOW INTERESTS ARE GAINED IN LENDING IN DEFI PLATFORMS

Using DeFi lending platforms, interests are earned through a process called “yield farming” or “liquidity mining.”

When you lend or deposit your cryptocurrency on a DEFI lending platform, you essentially provide liquidity to the platform. The platform pays you interest on your deposit in exchange for this liquidity.

The interest rate is determined by supply and demand in the market. The more people deposit funds into the platform, the lower the interest rate, and vice versa. This is because the platform uses these funds to provide loans to borrowers, and the interest paid by the borrowers is used to pay the interest to the lenders.

Yield farming or liquidity mining can earn even more interest on your deposits. This involves staking your funds in a particular pool on the platform and receiving rewards in the form of additional tokens or coins. The rewards are typically paid out to users who provide liquidity to the most popular pools on the platform.

In a nutshell, you can earn interest on your deposits in DEFI lending platforms through the platform’s interest rates, which are established by market supply and demand, and by participating in yield farming or liquidity mining to receive extra benefits.

BENEFITS OF DEFI LENDING TO ITS USERS

Decentralised Finance (DeFi) lending offers several benefits to its users, including:

- No intermediaries: DeFi lending removes the need for intermediaries like banks or other financial institutions. This means users can lend and borrow directly from one another without needing a third party to facilitate the transaction.

- Increased transparency: All transactions on the DeFi lending platform are recorded on a blockchain, making them transparent and immutable. This means users can verify the transactions and ensure that they are accurate.

- Lower fees: DeFi lending typically has lower fees than traditional lending methods, as there are no intermediaries involved. This can save users money on interest rates and other fees.

- Access to a wider range of assets: DeFi lending offers users access to a wider range of assets to lend or borrow. This can include cryptocurrencies, stablecoins, and other digital assets.

- Instant access to funds: Unlike traditional lending methods that may require a lengthy approval process, DeFi lending can offer users instant access to funds. This is because the lending process is automated and does not require human intervention.

- Increased control: DeFi lending offers users increased control over their funds. Users can choose who to lend to or borrow from, set their own interest rates, and manage their own portfolios

BENEFITS OF DEFI LENDING TO FINANCIAL INSTITUTIONS

Decentralised finance (DeFi) lending provides several benefits to financial institutions, including:

- Access to a Global Market: DeFi lending provides access to a global market of borrowers and lenders. Unlike traditional lending, where institutions are limited to their local market, DeFi platforms enable financial institutions to lend and borrow from individuals and organisations worldwide.

- Reduced Costs: DeFi lending can significantly reduce costs for financial institutions by eliminating intermediaries, such as banks, brokers, and clearinghouses. Transactions can be executed automatically using smart contracts, reducing the need for manual processing and paperwork.

- Increased Efficiency: DeFi lending can streamline the lending process, reducing the time and effort required to initiate, approve, and fund loans. Smart contracts can automate the entire process, from loan origination to repayment, reducing the risk of errors and increasing efficiency.

- Reduced Counterparty Risk: DeFi lending can reduce counterparty risk by using smart contracts that automatically execute when certain conditions are met. This eliminates the need for trust between parties and ensures that loans are repaid according to the terms of the agreement.

- Transparency and Security: DeFi lending platforms provide high transparency and security, as all transactions are recorded on a blockchain. This ensures that all parties have access to the same information and reduces the risk of fraud or manipulation.

CONCLUSION

DeFi lending offers financial institutions an all-around more effective, economical, and secure way to lend and borrow money. It allows institutions access to a global market, lowers costs, boosts productivity, lowers counterparty risk, and enhances security and transparency.