In decentralized finance (DeFi) and cryptocurrencies, the quest to generate liquidity and gamify protocols for opportunity has given rise to many protocols, with “DeFi bribes” being a notable dynamic.

This article delves into the meaning of DeFi bribes, the rationale behind the terminology, its connection to the “Curve War,” the pivotal role played by the Convex protocol, and the resulting impact on the DeFi landscape.

TABLE OF CONTENTS

Understanding DeFi Bribes and the Genesis of Curve Wars

Traditionally, a bribe involves offering something valuable to influence a decision. In DeFi and crypto, DeFi bribes are incentives, often tokens, that projects provide users in exchange for their support or participation.

In the world of DeFi, this isn’t too far from concepts like airdrops, liquid staking, or farming. So why is the term “bribe” used here?

Let’s delve into that.

Unveiling the Curve War

Liquidity holds significant importance in the DeFi space. Usually, platforms and protocols reward users with tokens for supplying stablecoins or more valuable assets as liquidity.

The curve finance protocol became a go-to place for new projects seeking liquidity due to its substantial stablecoin liquidity volume. Curves native token, $CRV, is distributed to liquidity providers.

Each liquidity pool receives a designated share of $CRV rewards, and when staked in curve finance, it yields $veCRV tokens.

These $veCRV tokens enable voting for additional $CRV rewards within the liquidity pool. More $CRV rewards attract more liquidity providers, making these rewards valuable in maintaining liquidity and yield for stablecoin projects, protocols, and marketplaces.

At the core of Curve Finance lies the pursuit of $veCRV tokens. These tokens can influence how $CRV rewards are allocated across various liquidity pools within the Curve ecosystem.

As projects sought methods to bolster their liquidity and offer attractive yields to liquidity providers, the competition for $veCRV tokens grew fiercer, leading to what’s now known as the Curve Wars.

The Curve War exemplifies how DeFi competition can trigger innovative strategies, including the concept of DeFi bribes.

Who Were the Key Players?

In this competition, Curve Finance was a central player due to its efficiency in stablecoin trading. Other projects, like Convex Finance, Yearn protocol, and StakeDAO, also joined the fray with innovative ideas that added to the rivalry.

Why Did the Curve War Happen?

Various factors fueled the Curve War. The rise of yield farming, liquidity mining, and governance tokens added to the race to get liquidity onto protocols.

Combined to dominate the decentralized exchange market and entice rewards, this made the competition intense.

The Birth of DeFi Bribes

The Curve Wars marked the start of DeFi bribes. Projects started offering incentives(bribes) to encourage users to provide liquidity, trade, and participate in governance(vote) for a specific liquidity pool, resulting in higher emissions earned by the pool.

This approach aimed to win users’ loyalty, boost protocol activity, and attract more assets to the platform.

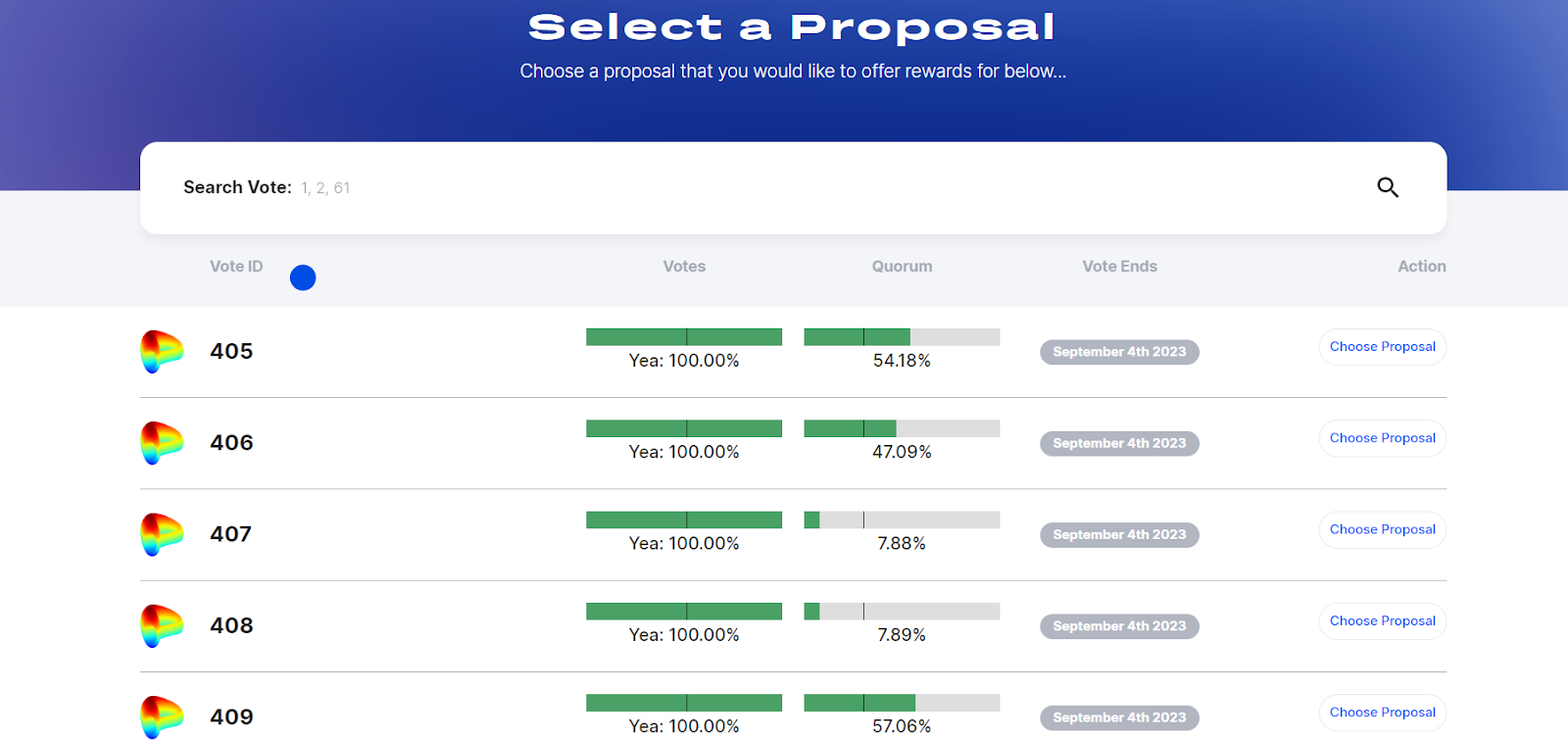

The proposal page of bribe.crv.finance. Source: bribe.crv.finance.

Convex Finance: A Product of Curve Wars and DeFi Bribes

Amid the Curve Wars, Convex Finance emerged, built on the foundation of the DeFi bribes strategy. Convex aimed to amplify yield for Curve Finance’s liquidity providers.

By encouraging users to lock up their $CRV tokens for a set period, they could earn additional $CRV rewards and $CVX tokens.

Convex fostered a rewarding cycle that benefitted all participants. $CVX holders also gained the power to vote on Votium, influencing which Curve Liquidity pool receives more $CRV rewards.

Source: Tokenomics 101: Convex Finance by Mason Fasco

Convex Finance acknowledged that not all users would commit to a four-year lockup period for maximum rewards.

To accommodate this, they provided equivalent rewards and the flexibility for $CRV holders to sell or withdraw at their convenience.

Convex Finance amassed over 57% of $veCRV tokens in no time, conferring significant decision-making authority within the Curve ecosystem, thus influencing the allocation of Curve’s rewards.

Several DAOs, including Terra, Frax, and Badger DAO, accumulated substantial Convex tokens ($CVX) in pursuit of controlling Curve’s voting power.

Exploring Convex Analysis and Bribe Rewards

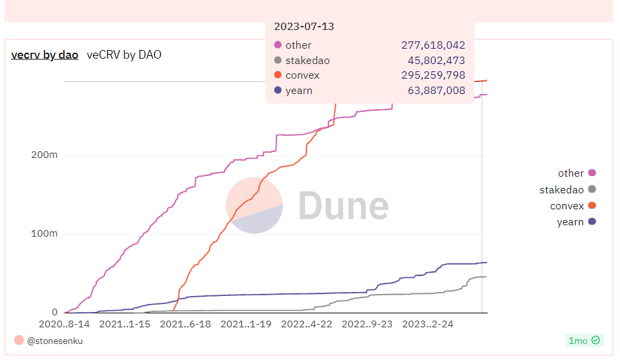

The amount of $veCRV (voting power) owned by DAOs, with Convex holding the highest voting power, can also be equivalent to the number of CRV tokens locked by each DAO. Source: @Stonesenku on Dune

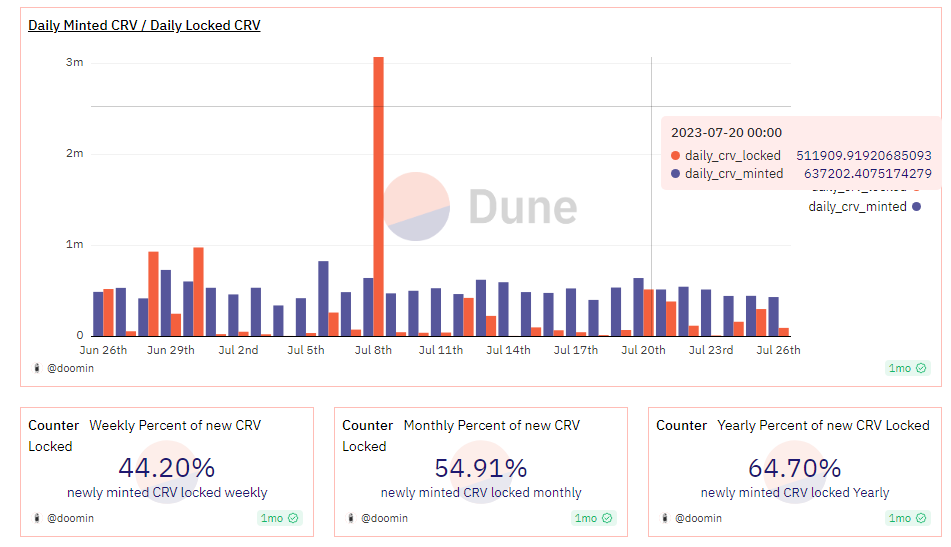

Minted $CRV compared to Locked $CRV across different time frames. Source: @doomin on Dune

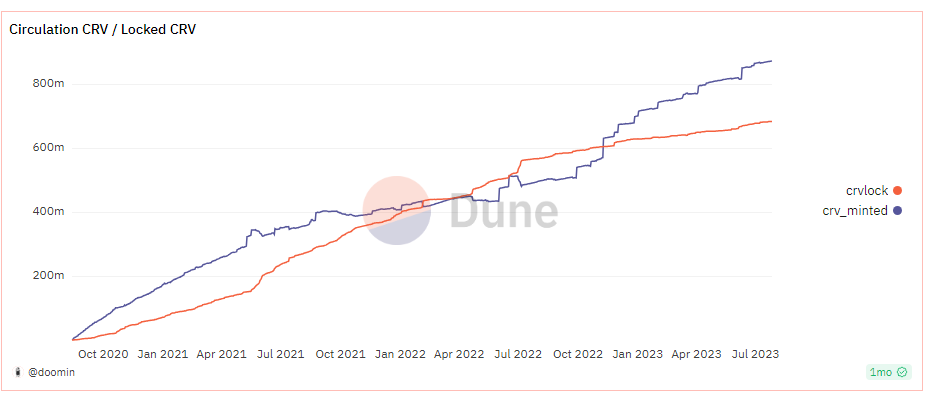

$CRV in circulation compared to locked $CRV Source:@doomin on Dune

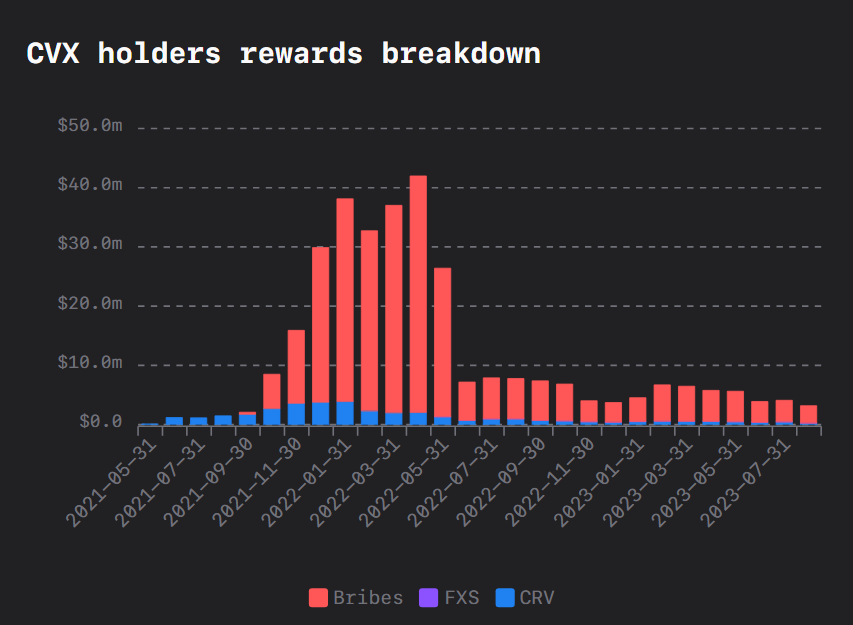

Bribes paid to $CVX holders holders over time Source: llama.airforce

2.6 million in Bribes was paid to $CVX holders for the month of August 2023.

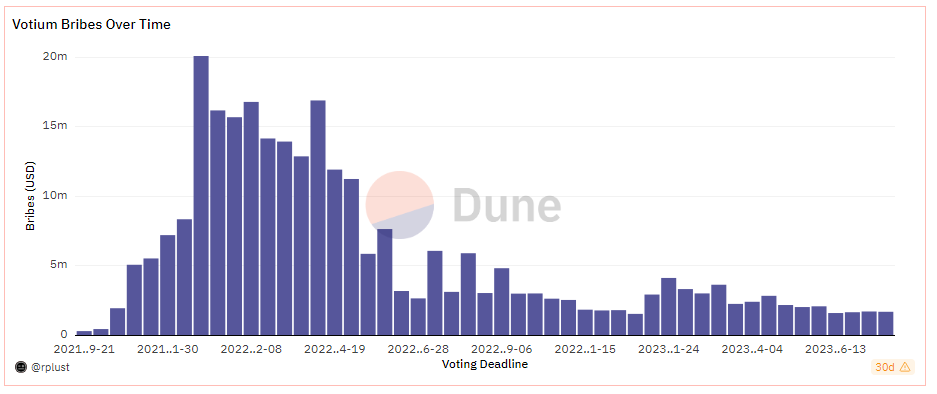

Bribes paid to $veCRV/$vlCVX holders over time source: @rplust on Dune

Over $1.6 million was disbursed in bribes to holders of $veCRV/$vlCRX for July 2023. This highlights the continuing profitability of the bribery strategy, particularly for the Convex protocol, which has consistently emerged victorious in the ongoing curve war.

This phenomenon also accounts for the daily increase in the number of locked $CRVs. The rate of locked $CRV exceeds that of newly minted tokens, standing at 54.91% every week and 64.70% annually.

To learn more about Convex tokenomics and how it works, check out the article: “Tokenomics 101: Convex Finance” by Mason Fasco.

Conclusion

DeFi bribes give us a glimpse into the creative strategies and intense competition within the DeFi world.

The Curve Wars demonstrated how incentives can shape user behavior, protocol development, and power distribution in DeFi ecosystems.

Convex Finance’s rise as a product of these wars shows how fresh ideas can emerge from competition, shaping the fast-changing world of decentralized finance.