I am a big fan of having my cryptocurrency earnings work for me, and one of those means was Liquidity providing (LP) back in 2021.

During the DeFi summer of 2020, LP played a crucial role in the growth of decentralized exchanges (DEXs) by addressing their long-standing liquidity challenges. LP has been a concept in the finance world for a long time and its application in DeFi was a natural progression. The growth of DEXs and the success of LP in DeFi helped to expand the ecosystem, leading to the emergence of newer DeFi protocols and applications, which some people call Defi 2.0.

Defi 2.0 is a phrase in the blockchain world that refers to a subset of DeFi protocols built on prior DeFi breakthroughs like yield farming, lending and other things.” as stated on Cointelegraph.

After many hacks in the past on Defi protocols promising high yields for providing liquidity, borrowing or lending on their platform, I personally shied away from Defi protocols a little bit more like a break, but I stuck with staking on POS(Proof of stake) blockchains.

This article will discuss a Defi protocol; Archimedes Finance, a lending/borrowing marketplace.

Hop in for the ride!

TABLE OF CONTENTS

- WHAT IS ARCHIMEDES FINANCE?

- UTILITY, GOVERNANCE AND STABLE TOKENS OF ARCHIMEDES FINANCE PROTOCOL

- FEATURES OF ARCHIMEDES FINANCE – DIFFERENCE FROM OTHER BORROWING AND LENDING PROTOCOL

- RISK OF USING ARCHIMEDES FINANCE

- HOW TO PROVIDE LIQUIDITY ON ARCHIMEDES IN A FEW STEPS

- HOW TO OPEN AND CLOSE A LEVERAGE POSITION ON ARCHIMEDES IN A FEW STEPS

- CONCLUSION

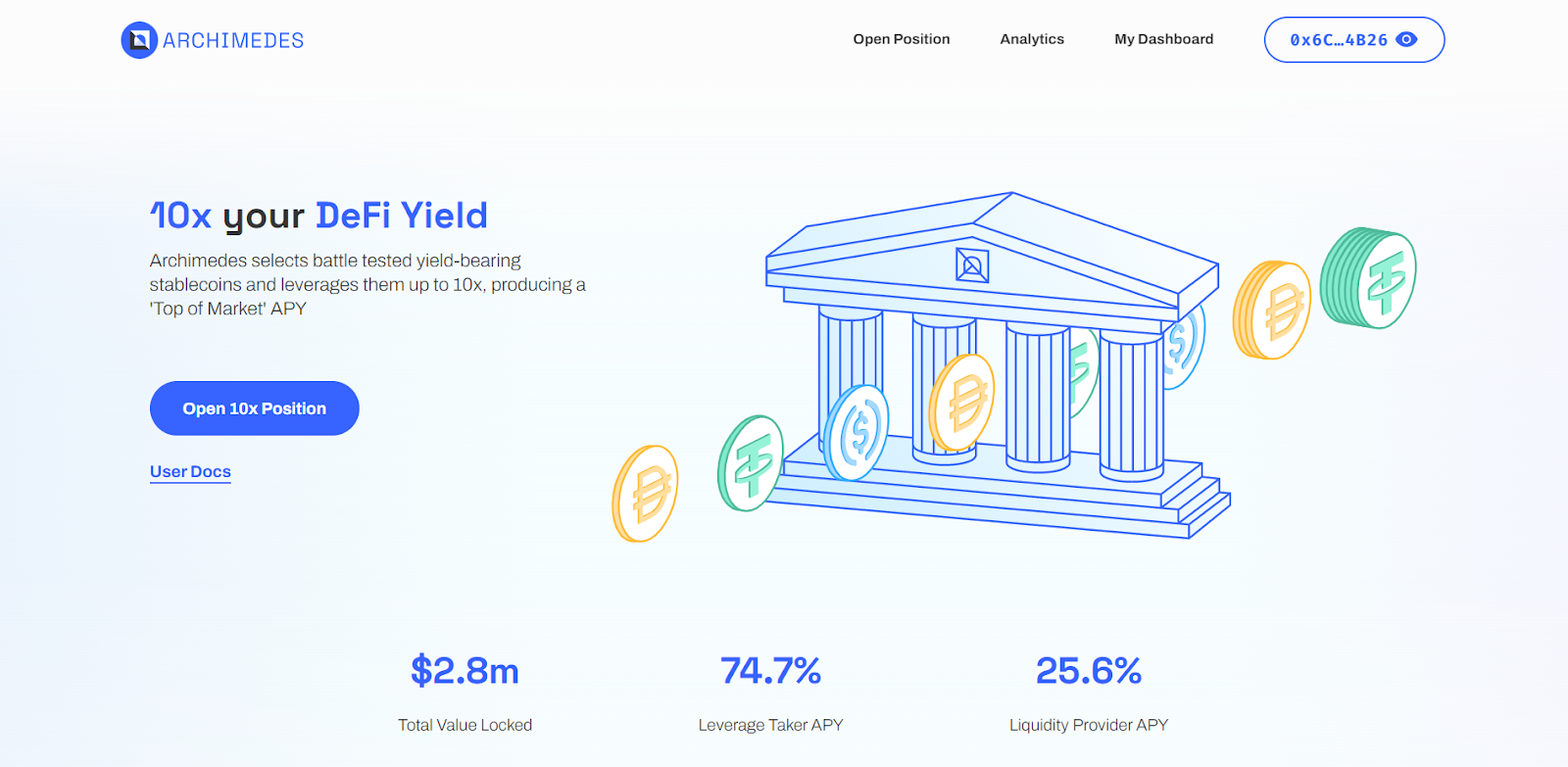

WHAT IS ARCHIMEDES FINANCE?

Archimedes is a decentralised lending and borrowing marketplace that allows investors to deposit assets and use them as collateral to create leverage positions in other to borrow a stablecoin, lvUSD.

These leverage positions are purchased using ARCH tokens.

Archimedes finance assures Liquidity Providers(LP)/ lenders high earn and stable APY.

Borrowers (Leverage Takers) earn up to 10x yield of what yield-bearing stablecoins such as OUSD offer.

Archimedes finance

UTILITY, GOVERNANCE AND STABLE TOKENS OF ARCHIMEDES FINANCE PROTOCOL

ARCH; A governance and utility Token

ARCH tokens are used to secure or purchase your leverage opportunity. This simply means your collateral can not be leveraged, and investors can not borrow IvUSD if investors don’t pay an upfront fee in ARCH to access the leverage.

The protocol distributes a limited number of ARCH tokens to our Curve LPs. They lend the funds, thereby holding the “ticket to leverage”, and LTs must buy ARCH from LPs.

An auction determines the amount of leverage 1 ARCH gives access to. The more demand for leverage, the more demand for ARCH.

lvUSD is a synthetic USD-pegged stablecoin. lvUSD represents “potential leverage”.

The protocol borrows it from LPs to lend it to LTs and swaps it with 3CRV, which is then swapped with OUSD to gain leverage.

FEATURES OF ARCHIMEDES FINANCE – DIFFERENCE FROM OTHER BORROWING AND LENDING PROTOCOL

Archimedes was built on top of Curve and supported it.

The fixed CRV token emission is limiting the growth of Curve finance, and all the pools will have to share the same CRV reward been emitted.

This means that each liquidity pool gets a smaller share of CRV for all investors and projects that use Curve.

It is well-known that when a pool or protocol is highly competitive, its reward drops.

The bigger the TVL (total volume locked), the lesser the rewards; this is because Defi protocols typically use a fixed emission schedule of their governance token as rewards for their liquidity mining programs.

Most of these rewards/ defi tokens are not even backed enough with the utility to withstand the slightest sell pressure, not forgetting that the lesser the reward, the less attractive the pool becomes to LPs.

But for Archimedes’ finance, it’s utility and governance token ARCH has been designed as the only access to leverage to promote a healthy ecosystem, with a cutting-edge token emission design, a real yield approach and a diversified APY.

The protocol collects three types of fees which are sent to the Archimedes Treasury to be used as rewards for the 3CRV/lvUSD Liquidity Providers:

RISK OF USING ARCHIMEDES FINANCE

Just like every other Defi protocol, Archimedes Finance has risk similarities such as losses due to liquidations, smart contract exploits, and de-pegging of the stablecoin, which is governed by economic conditions involving other currencies.

In this case, the stablecoin of Archimedes finance is IvUSD, which is a synthetic USD-pegged stablecoin.

Archimedes’ loan is always fully collateralised, and everything takes place inside the protocol so that collateral never leaves the Archimedes vault.

The risks associated with Defi products are numerous.

Archimedes has designed its tokenomics and mechanisms to mitigate those risks to the best of its ability.

You can check out the product risk in Docs.

Curve Pool Imbalance Risks (and lvUSD Depeg), Underlying Assets Risks, and Smart Contract Risks associated with Providing Liquidity.

Liquidation Risk, Underlying Asset Risks, Variable Fees Risk, and Smart contract risks are risks associated with Leverage Taking.

HOW TO PROVIDE LIQUIDITY ON ARCHIMEDES IN A FEW STEPS

WHY USE ARCHIMEDES FOR LIQUIDITY PROVIDING

- Archimedes is designed to provide high, sustainable rewards and diversified returns from revenue share; this comprises three fees (Leverage Fee, Origination Fee and Performance Fee), Low Risk/Reward.

- Archimedes’ Liquidity Pool differs from other Curve pools in that its APY is primarily achieved with dynamic emission rewards from our native ARCH token and, on a lesser scale, the standard Curve pool CRV rewards.

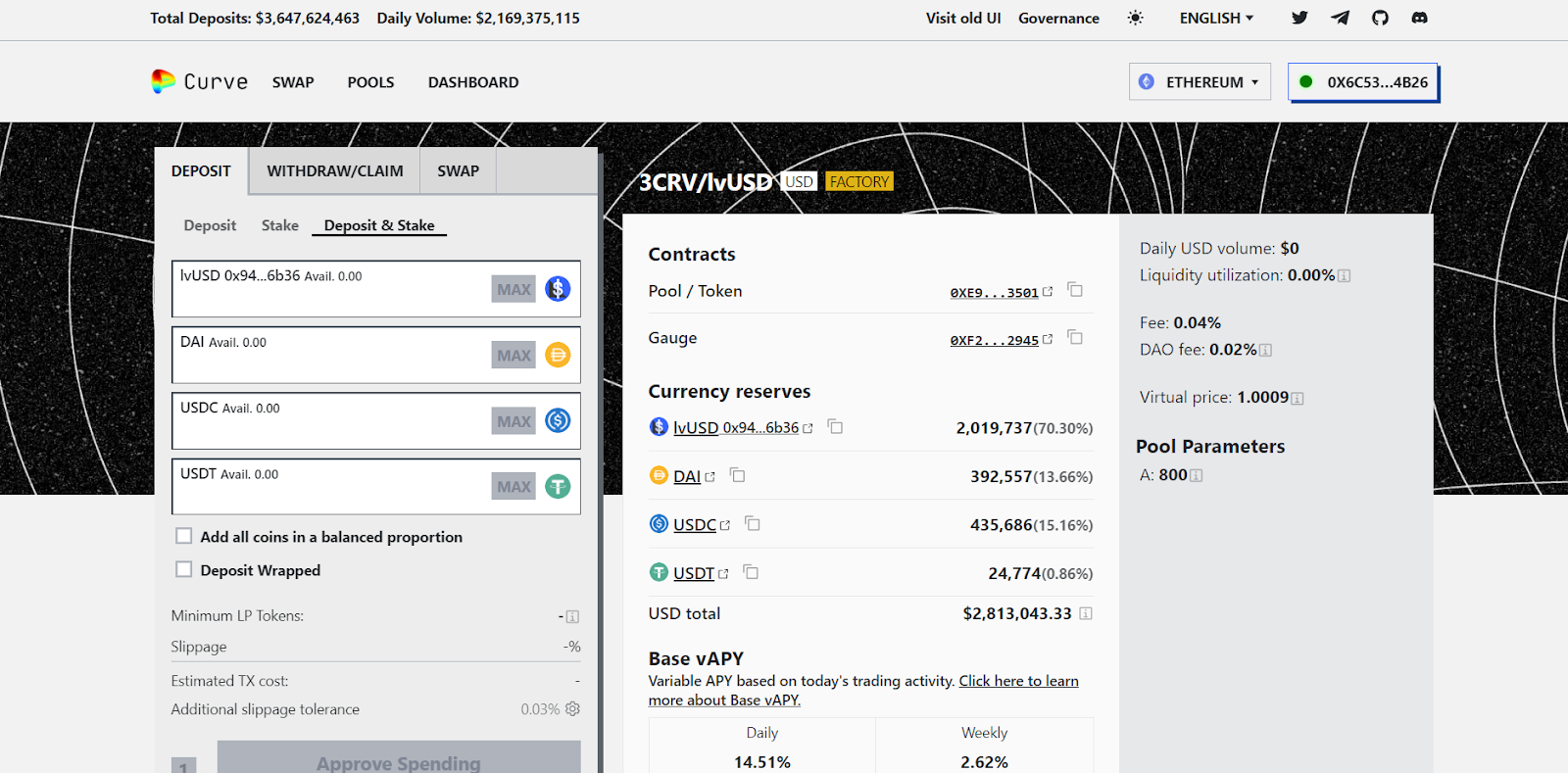

HOW TO PROVIDE LIQUIDITY ON ARCHIMEDES

Investors must deposit one or more of these stablecoins, DAI or USDC or USDT, into Curve liquidity pool.

Follow the Archimedes’ Steps to provide liquidity

Archimedes Liquidity Pool On Curve Finance

HOW TO OPEN AND CLOSE A LEVERAGE POSITION ON ARCHIMEDES IN A FEW STEPS

WHY USE ARCHIMEDES FOR TAKING LEVERAGE(BORROWING)

- Leveraged asset base APYs are constantly changing (like the entire market). So adding high leverage helps keep your position at the top of the market regarding APY.

- Archimedes offers top-of-the-market APY on stablecoins—get x5 to x10 leverage on an average APY appreciating stablecoin.

- Archimedes packages your position in an NFT, so investors can trade it on NFT marketplaces without unwinding it.

- Leverage allocation is limited, and many people may be willing to pay a premium for your position NFT.

- The high-quality assets that Archimedes uses for its collateral create less risk for your funds.

- Leverage takers must pay all their fees upfront when they open a position. This makes it easy to keep track of variable interest payments over the position’s lifetime.

HOW TO OPEN A LEVERAGE POSITION ON ARCHIMEDES

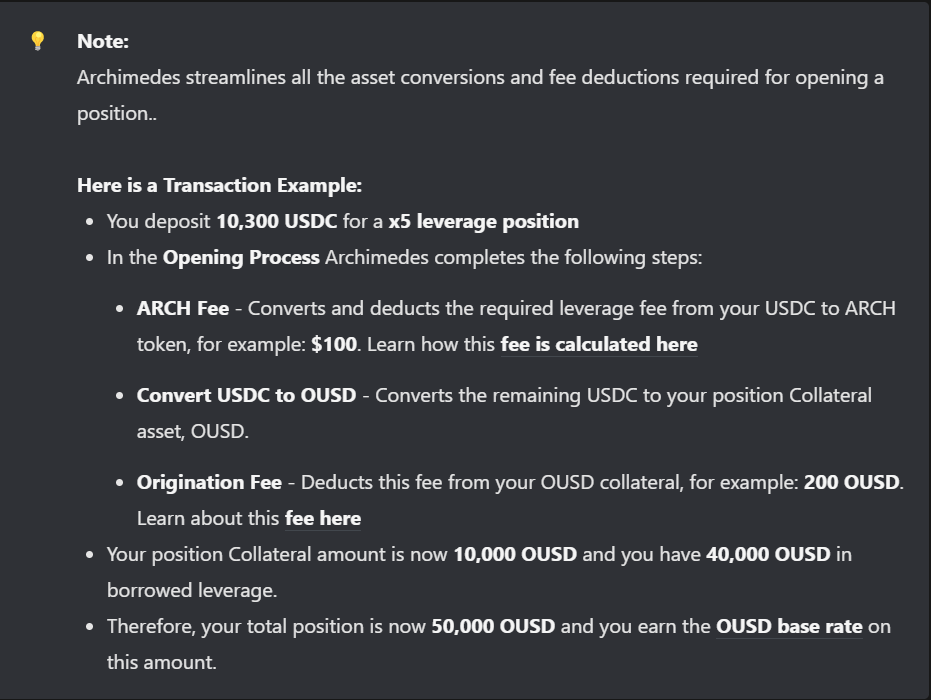

Investors will need to open a leveraged position in either of the stablecoin USDT, USDC or DAI.

Archimedes has made it easier to help investors to convert stablecoin to OUSD and ARCH; the exact amount of OUSD and ARCH needed for opening a position will deducted from your stablecoin. Which means you mustn’t have them. check out the example below for more clarification.

Archimedes’ example for opening a leverage

Follow the Archimedes Steps for Leveraging Positions

HOW TO CLOSE A LEVERAGED POSITION ON ARCHIMEDES

There are three ways in which positions can be closed:

- Investors can close positions at any time.

- Investors can wait for positions to expire and then claim the funds.

- Investors can sell their NFT Position on the NFT marketplace like Opensea.

NFT of a leveraged position with a total position 7.7k OUSD will expire; on 4 MAR, 2024

Different methods and steps for closing positions can be found here

CONCLUSION

The best thing about decentralised finance is you are your own bank, but it comes with the stress of having to manage everything yourself, including your safety in the space, regardless it is a fun place to be.

I will just end with this note, do your own research (DYOR) and be your own bank (BYOB).

Thanks for the insight bro..